Concept: Chain Purchasing For Retirement Cash

- To play you must have the cash to make a commercial real

estate purchase, to rehab it as needed, and to wait for it to get

rented up and stabilized. The concept assumes, in addition to the cash,

you are capable of finding a bargain, closing a deal, carrying

out the rehab, and getting it filled with renters.

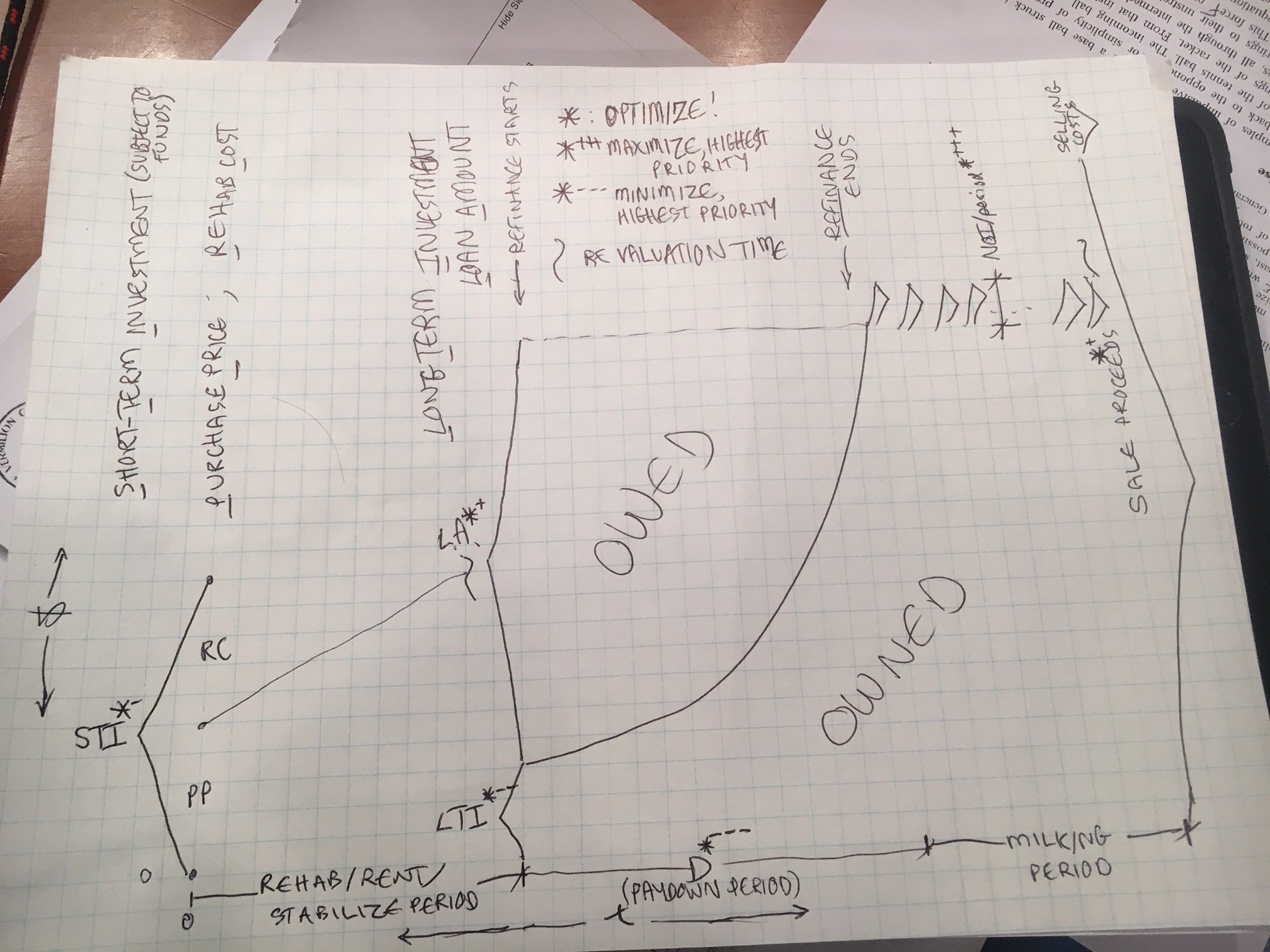

- Then: spend your STI, Short Term Investment money like this:

- Buy your bargain at Purchase Price PP, which you spend all at once.

- Rehab, rent, stabilize at Rehab Cost RC, which you spend gradually.

At this point, before D starts, you should have added a lot of value

to the property. Since public developers like Quadrant Homes report

gross margins of 40 percent, it means they paid 60 percent for something worth

100 percent. Maybe you won't do that well, but do your best.

- Next: take your numbers to the bank. They often lend 75% of the

stabilized value, which remember you paid as little as 60% to

create. (Do this in advance, so you know what to expect.)

- Hitting these numbers means your LTI, Long Term Investment,

is -15%, which is money out instead of money in. It is like getting

money out on a flip, but you still have the property in your hands.

A negative LTI means you got more out of the refi than you invested

in the first place. Sweet.

- Now take that money and start this

algorithm again at the top with another property, on another chart.

Repeat as much as you have time and capital for, which might be

forever since there is always a bargain somewhere and since your

capital may be increasing at each cycle.

- Don't forget that the

money you get out of the refi is loan not income so there's no tax

on it, so you actually have the 75% in your pocket to work the next

deal with, instead of losing a fat chunk to taxes. Because you pay

income tax on income, not on loans you take out.

Meanwhile keeping our focus on this property....

- Instead of paying the scheduled minimums, accelerate the mortgage

payments so that instead of taking 30 years, it takes D years. For

example, a single monthly payment, doubled, at the beginning of a 30

year mortgage, brings forward the paid-off date by much more than

one month

A single extra payment at the beginning of a 30 year loan at 15%

annual interest brings the paid-off date forward by 55

months. On a loan at 10%, that payment brings it forward by 18

months; between 8% and 2% the integer interest rate is approximately

the number of months saved, so 8%, 8 months, 6%, 6 months, roughly,

according to my spreadsheet.

This means, after reserves, don't take your extra

income and pocket it, do pay down the mortgage, just as fast as you

can. The point of this model is to make D be short. D=5

years is excellent. D=10 years is barely acceptable. D=3 years is

achieveable if you are a rock star. And yes it is achieveable.

Short D means you have a money machine that pays off soon. It

throws off lots of cash relative to its price. Cash gets your

equity up to 100% fast, and throws real cash at you forever after.

This is the whole point of investing, duh.

Footnote: Some people think you should never pay off your real

estate. I disagree. There is a role for mortgage money, and a

role for being paid off. The role for mortgaging a property

is to get your money out of it immediately, so you can rinse

and repeat and do another one as soon as possible. The

role for being paid off is now you get 100% of the income from

the property to your pocket for your own actual use. That's

what we want, right? Money we can actually use in our

lives.

The point of smart investing is to buy cashflow. Buy

something that will pay for itself over and over, not so that

you can quick go supine under some banker again, and typically

take risky, risky risks. Instead, be the top gun with the

paid off mortgage and that money stream going direct deposit.

The bank seeks to eat most of the money stream with the least

of the risk, because if the income dries up to just enough to

cover the mortgage, they still win while you get nothing.

Incidentally, what did it cost the bank? They do fractional

reserve banking, don't you know about that? Somebody has an

account with them with $10k in it, the bank invents 90k out of

thin air and makes a loan of $100k, because it's 10%

fractional reserve. Look it up, I am completely serious. Then

the 5% interest they are getting paid on that 100k loan gives

5k/year net proceeds to them. Why? Because SOMEONE ELSE put

10k in an account with them. Banking is sweet, don't you get

it. Don't go under a banker except to dramatically improve

your situation. Don't do it except to buy something that

generates EQUITY in a HURRY and then CASHFLOW FOREVER.

Yes, mortgaging ONCE so you can get a whole added property for

nothing (LTI<=0) that will pay off in 3-10 years and pay you

its value over and over forever, okay that's worth while, as a

temporary position that enables you to do it one more time,

to multiply your income stream by doublings, property after

property rather than squeezing out an interest arbitrage of a

few percentage points. Okay! -- if enabling a sequence of

purchases, yes. But I say, one time, once per property,

because that is enough to make a sequence of properties, one

after the other. In math this is called, Countably

Infinite. One after the other, no limit. Isn't that good

enough for you? Do you have to ask for more than Infinity?

If you want to continuously remortgage that property after it

pays off then why are you doing it? When are you ever going to

start seeing the benefit?

Maybe you're young and dumb. I'm 56, and if it doesn't pay

off before I retire, then why am I doing it? If D=30 years

like a regular house on a 30 year mortgage, I'll NEVER see the

benefit. I say, get around on the other side of the issue.

After 1x, the mortgage has already done its job. It let you move on

to the next for $0 in, that was its job. After D comes the Milking

Period. Just save, put the money in your pocket, don't be in such an

idiot hurry. Pretty soon you'll be able to buy another anyway, if

you're just a little patient. And if it takes too long, you're not

patient enough, then the lesson is you just didn't find the right

bargain in the first place for D to be small enough. The lesson is

not that you need to hurry back to the banker for a fix.

Do you get it? The day I paid off my mortgage, my net income POPPED!

It went from a hundred or a few hundred measly dollars to $3500 a

month! It doesn't make me rich but it meant I retired from plumbing

the next day. Who likes mortgages? Banks do. Do you get it? Use

them when YOU win, not when THEY win.

Okay, back to our main story line.

- After each period of time (month or year) it throws out a net

income of NOI/period (e.g., $3500/month). Once the mortgage pays

off, you now get direct income to your pocket of that amount,

that often. So:

- What did it cost you? Time And Money. D years of time you

had to wait. Aim for short. And Money? It only cost you your

STI amount and only during the initial buy/stabilize phase,

which might be as much as you can safely afford, but after the

refinance, then your long term cost might be negative with money

added to YOUR pocket, or zero, or if LTI>0 hopefully at least it

is a fairly small value.

- What did you buy? Money After Time. Regular income of

NOI/period for every period starting after D.

- The Goal: Minimize D, and Maximize NOI/Period, while keeping

LTI zero or negative. STI is as much as you can afford, and after

refinance, you can do it again, and again.

- At this point my personal investment model stops. All I want is

income, and I don't care what the resale value is. Frankly I bought

the property for nothing (LTI<=0), so I don't care what I sell it

for. My estate can sell it, if they want. What I actually do care

about is how long do I have to wait to start getting paid (D), and

how much do I get every month or year forever as income

(NOI/period). I'm not going to sell it, I'm going to retire on it.

- You on the other hand might sell it, then you'll pay Selling

Costs SC, and extract Sales Proceeds SP.

Great. Put it into your

model.

Why do it?

Why not? If...

- IF STI is within your means AND

- IF LTI is insignificant or negative AND

- IF D is reasonably short, AND

- IF NOI/period is valuable enough to motivate you to aim for it THEN

This can work. That's all I'm saying: Yes, It Can.

Me, I want D<5 years. That's the whole measure of the quality of a

deal, how long is D? If the property will throw off cash at a rate

enough to pay off, in a short time D, a mortgage of 100% or more of

the cost of buying and repositioning it, then that it works for me.

Indeed: Why Not!

Risks: Reasons to Consider Why Not

- Money loser property? You need to know your purchase,

rehab, and operating costs, and rent ranges, and vacancies at least

roughly to have confidence in the plan. So do homework to eliminate

this risk. Yes you have to do actual homework and know.

- One Property Fails? If your loan is non-recourse and the

property becomes owned by the bank, the others in your chain keep on

rocking. Since it cost you nothing (if LTI<0), where is the loss?

- Bad operations? Get multiple eyes on it. Hire a coach for

a review of your numbers and processes. Get competitive quotes.

Vigilance. Hire someone to send you photos or a walk-through video.

Hopefully you have enough margin in the deal that you can afford to

make some mistakes and learn. If D<10 and you are awake, you should be

fine.

- Economic downturn during project? This is the big worry.

You may have paid too much compared to the coming trough but the real

question is, Do you care? .. Because you own a property that pays for

itself and covers its own mortgage by a fat margin. Once financed on

comfortable rent projections what is the actual risk? That D will

last a little longer? You may have to postpone retirement, but you

haven't lost your retirement. It's really, you aren't actually

losing money, just waiting a bit longer. With the relative stability

of rents in a down market, and your financial homework on day one,

it'll still pay off, it'll still survive, and you'll survive. On the

other hand, compare the risk of not having done that deal at

that time so that your calendar would start later and it pays off

later. A later payoff from that cause is no different from one caused

by a lowering of rents or an increase in vacancy, which you should be

prepared to handle, with a margin of error in your plans. Since the

cost of delay is also significant, consider if you found a deal today

at the teetering edge of a market fall, won't the numbers still work

where they work? If so, so do the deal, get your money out quickly if

you can, and maybe there will be even better deals later during the

trough.

- Re-Financing risk. If you are all in but the refinance

fails: let's game this one out, and see what is the problem. So, yes

you don't get your money out to do another deal instantly. Yes, your

larger short term investment STI just became a larger long term

investment LTI. But at the same time you just reduced D to zero and

started putting rents in your pocket sooner. It isn't multiple free

streams of cash, but it's one, not a stick in the eye. Yes your

capital is tied up but it is producing a distinctly pleasant interest

return, more than enough to pay the mortgage, so much more that you

could have accelerated payments to end in only D years and now, instead,

all of that is

now coming to you instead of going to a bank. There is no actual out of

pocket loss. The only "loss" here is the opportunity cost in the

imaginary world where you could have gotten your money out right away

to do another and another. Well, we all knew the ride might end and

the job is to ride it while we can, then the jig is up when it's up,

it's the best we could do. Is the nonavailability of future

opportunities a reason to not take advantage of a current opportunity?

Duh, no!

- City risk. If the jobs leave town, no renters. Yes

that's possible, remember Dakota fracking man camps. So find

multi-employer towns! However, mostly, in the US, places are

stable to very slowly declining. And if money leaves town,

owners may become renters coming toward you rather than

emigrants running away from you. Landlording is actually great

business during a downturn, when home ownership falls. You just

have to be a little better than the alternatives, so paint,

polish, plant some flowers, and answer the phone on the first

ring. You are at least a player in a stable market. Run on the

top side of the ice, don't be all depressed and giving up.

Those who work tend to receive their reward.

Conclusion

I am making some somewhat controversial arguments, against both the

keep-refinancing-forever mentality and the

leverage-at-the-start concept, which seem pervasive.

First, infinite refinancing trees (multiple branching refinancings on

each property) are for the benefit of bankers at the cost of those who

just want to be rich. Establishing a fat lifetime income ought to be

plenty for anyone, don't you think? I do believe in mortgage

financing as a way to multiply your wealth-creation efforts, once is

enough for each property, as a basic approach. That still gets you

(countably) infinite returns. You can do your scale of deal over and

over and over, without limit, and get as rich as you want. Whereas

refinancing after payoff just benefits the bankers who take the least

risky income tranch and leave you with all the risky leavings.

Instead, get fat at your own trough, be a tiny bit patient, and grab

those not-so-risky incomes for yourself. If you have to get even

fatter then save that too, retire even later, and buy more off your

increased savings.

My second controversial position is against starting with no working

capital. Lots of investors think you should leverage from the start,

whereas I argue that you should borrow AFTER buy/add-value/stabilize.

My backwards approach, based on adding value, allows the mortgage to

give me more than I put in at the start, allowing me to chain onward

to other properties, each of which will end up costing me

approximately nothing (where LTI<=0). If you are able, why not? So

yes, save and create some foundation of capital to work with. Yes,

shop till you drop to find a great bargain. Yes, leverage it

creatively to 100% or more, but AFTER it stabilizes as an income

stream. Those are not risk-creating events, in deals where D is

short. But if you want to borrow the short term investment amount

(STI) used initially to buy and reposition and stabilize the

investment, then you expose yourself to a period of market

vulnerability. Typically that money will be borrowed from hard money

lenders, where 1%/month is typical, and if the market drops or pauses,

you may find yourself working for nothing, or bitten by loss of

whatever fraction you did put in, or waiting until their fat interest

rates eat up the whole project. Sure, you may know what you're doing,

and most of the time you may be lucky that market conditions don't

change during the project. But especially if you make a practice of

this borrowing before the buy, then some day there will certainly be a

fall before the refi, and you will be at the mercy of your first-day

lenders.

These are the reasons I consider this a valid investment model. If

you have your act somewhat together, then certainly you can learn what

you need to know to make reasonably valid projections, you can find

bargains, and you can dive in and spend that rehab money carefully

(more carefully since it's yours, and therefore much more profitably),

you can

make a great, performing rental property out of it, on which most bankers

would love to give you a fine appraisal and mortgage, and after D

years from this mortgage date for just this property, you'll see

lifetime income coming through, plus the next one and the next one ad infinitum. I

don't see a lot of risks, and it gets me where I want to be. What

about you?

*: I'm a certified plumber, not a certified investment adviser. These

are opinions that make sense to me, and I'm sharing them for the

public benefit, if there happens to be value in them, but this is

not a warranted investment product, and you have to make your own

grown up decisions based on what makes sense to you, not what some

plumber told you in his investing blog. The legal truth is: Get

professional advice before action. The moral truth is: take

responsibility for your own understanding, and make decisions that

are your own. Did I need to say that?

|